Atlantis Asset Management

5 Penn Plaza, 14th Floor New York, NY 10001

(212) 256-1150

As a follow up to our last market commentary, I wanted to clarify where we are in terms of the overall market cycle, and then discuss our view of the market’s prospects and direction over the longer term.

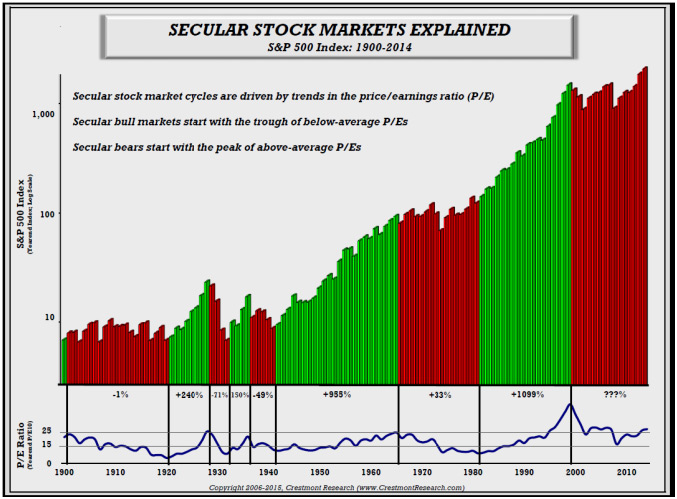

We view with amazement the clockwork cyclicality of the markets. Long term bull markets and bear markets have lasted anywhere from 10 to 20 years, or an average of 15-16 years, over the last 100 years. The chart below illustrates this cyclical pattern at work and indicates we have been in a primary bear market since the peak in 2000. Now 16 years into a flat to down (red) period, equity returns have been subpar at best. As of this writing, the S&P 500 index has appreciated only 23% in price terms since 2000. If we include dividends, the total return is 65%. While this disparity may seem unusual, it is not. Over the last 100 years, through bull and bear markets, close to half of the average annual return of the S&P 500 has been through dividend payouts. Investing during a primary bear market is a matter of survival. In times where capital appreciation is low, dividends provide a buffer to an anemic stock market. We believe equities are most likely nearing the end of this long term bear phase, and a new bull cycle is on the longer term horizon.

Chart courtesy of Crestmont Research

As shown in the chart above, the longer term cycle has lasted now 16 years, which leads us to believe we are in the late innings of this cycle. On a positive note, once this bear market is over, the last two primary bull markets lasted over 18 years, and the equity markets increased tenfold in each.

Within any market cycle, there are always shorter term corrective phases corresponding to the purge of excesses that inevitably occur somewhere in the global financial and economic system. This happens on average about every four years, whether the primary trend is up or down. The last 20% correction in the S&P 500 was in August of 2011, around the time of the downgrade of US debt, so we were overdue based on the four year cycle for a downturn in the market. This latest corrective phase, as we discussed in our last letter, is the result of a massive slowdown in China, which was on an unprecedented infrastructure building binge over the last couple of decades. For example, China was the eighth largest economy in 1995, just in front of Spain, and is now the third largest economy behind the US and the EU. This spending on all the raw materials required for a massive infrastructure build, lifted all boats, especially industrial commodities, and was a major engine for global growth. However, China’s slowdown is just one piece of the puzzle that leads us to believe that we are in the final stages of this long term bear market.

Within this bear market context, for the last eight years, worldwide central bank induced low interest rates have fueled a “liquidity driven” rally in all asset classes (bonds, stocks, real estate, and commodities). In the slower growth developed economies, investors and traders have been able to borrow money at almost zero interest rates to invest in higher yielding financial assets (the carry trade), pushing all assets with either true organic growth or decent dividends, higher. (It’s been a classic tale of inflation in wealth storing assets where too much money is chasing too few goods.) This liquidity driven rally, however, began to show the first signs of unwinding in 2014 within the commodity sector, through dramatically falling commodities prices. As China slowed their massive infrastructure spending, the prices of raw materials (commodities) began to sink. If the consumption level of all commodities was 100 billion dollars per day in 2014, today, at the same level of consumption, the values of those commodities is now only 55 billion. That is an almost 50% drop in the incomes of commodities producers across the globe. In percentage terms, it is functionally a huge withdrawal of global liquidity.

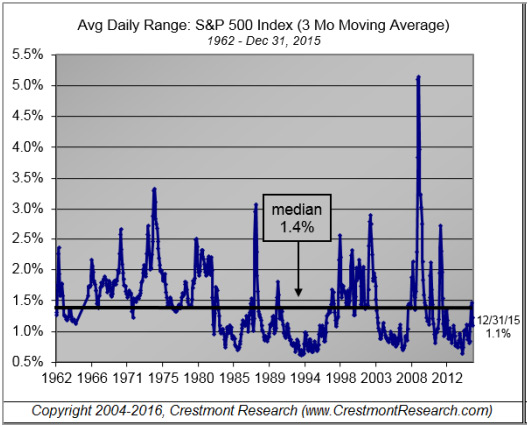

Chart courtesy of Crestmont Research

Capital now is fleeing at a rapid pace from the countries and the companies of commodity producers, and the fallout soon begins to impact other sectors, reverberating down the economic food chain. When incomes decline, borrowing grinds to a halt, thus a meaningful contraction of credit conditions occurs. The housing credit bubble, which started popping in 2007, was mitigated (reckoning postponed) by zero interest rates and quantitative easing. However, the plague of easy money is now claiming its next victim, the commodity producers. Deflation and China fueled overcapacity just finally caught up with them. During these times of dislocation, uncertainty reigns and markets go down. Because the prices of financial instruments reflect the expectations of future events, when prevailing expectations about the future are perceived suddenly to be highly uncertain, the markets inevitably adjust themselves lower.

One of the characteristics of every bear market nearing its end is a prevailing attitude of despair and general economic malaise. It is very hard to see, with all of the prior economic engines on a slower trajectory, where the next growth theme is going to come from. At these moments, the markets seemingly act in violation of conventional wisdom. The volatility (movement of prices up and down on a daily basis) in the markets has turned higher but, in perspective, we have just gone from an extended period of volatility being very low recently, are still below the average of the last 50 years. View the chart above. If you note, the last major bear market (1966-1982) had a much higher average volatility than the recent bear market (2000-201?). Volatility creates opportunity. When volatility starts going higher it is a signal that there will be a buying opportunity in the near future. We believe that this next opportunity will be a good point to reassess asset allocations and prepare for a long term bull market in equity valuations and prices. It is not there yet, but soon.

We believe how this will play out is; it is most likely that the prices of commodities will stay too low for just too long. There will be headlines about big company or even country debt failures. There is a heated currency battle going on, and currencies will be pushed around, and adjust at a disorderly pace. This will cause a lot of capital movement and the subsequent hand wringing. At some point, invariably, and we think in the near future, these dislocations and uncertain new realities will cause emotions to overtake reason. The equity market valuations (price to earnings ratio) will go down far enough to create a compelling long term investment opportunity.

As always, we invite all comments and would enjoy a discussion on anything about this article, or anything financial.

Sincerely,

Michael D. Cohn

Atlantis Asset Management LLC

Posted in: Blog